An Introduction to Stablebanking: A Guide to the Onchain Value Chain

This article explores the Stablebanking model that empowers fintechs and developers to build modern financial products using stablecoins and smart contracts.

Stablebanking is redefining finance by transforming digital dollars (stablecoins) into a programmable, transparent, and efficient financial system built on blockchains. Unlike traditional banks, it combines centralized regulatory compliance such as KYC and KYB with decentralized programmability.

This new model is expressed through a robust ecosystem of interconnected layers that enable stablecoins to flow seamlessly across the entire financial lifecycle: issuing, saving, investing, exchanging, and paying, all onchain. Understanding this value chain is critical for developers, fintechs, and investors aiming to build or capitalize on the future of onchain finance.

In this article, we unpack the Stablebanking ecosystem, revealing how its layers work together to power a new financial paradigm.

Beyond Payments: The Power of Stablebanking

Stablecoins started as a way to peg digital assets to stable values, like the U.S. dollar, enabling fast and low-cost payments. But their potential goes far beyond. Stablebanking replicates the efficiency of tokenized deposits, challenging legacy banking rails.

For example, companies like Circle are pivoting from pure issuance to tech platforms, using tools like the Cross-Chain Transfer Protocol (CCTP) to enable seamless money movement. Tether, meanwhile, operates more and more like a traditional bank, leveraging scale and collateral flexibility. These shifts signal a broader trend: stablecoins are becoming the backbone of a new financial system.

Stablebanking’s real power lies in its ability to:

- Eliminate friction: Settle transactions instantly at a fraction of the cost of legacy systems.

- Enable programmability: Use smart contracts to streamline workflows like payroll, rewards, and yield strategies.

- Ensure transparency: Leverage onchain compliance solutions, such as Chainalysis, that exceed the capabilities of traditional AML tools.

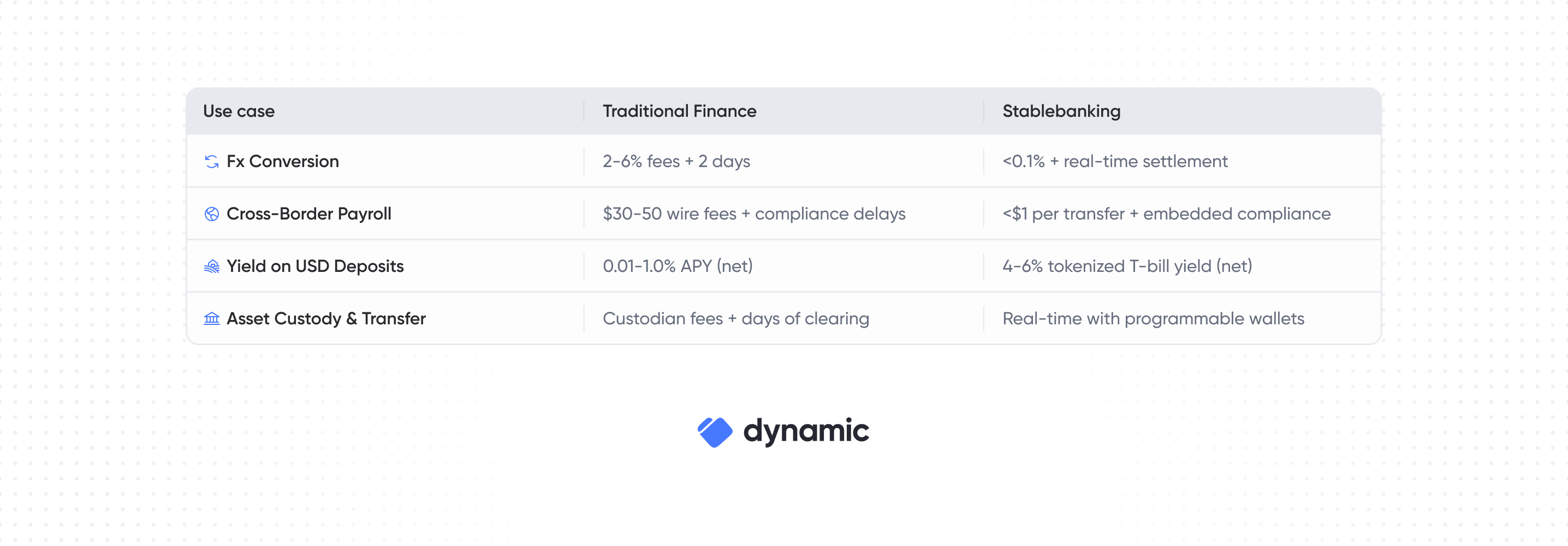

Why Stablebanking Outshines Traditional Finance

This model blends the oversight of traditional finance with the openness and efficiency of blockchain infrastructure. By combining regulatory safeguards with transparent and programmable systems, Stablebanking turns compliance into a feature, not a limitation.

Here’s how it stacks up against both legacy systems:

The Stablebank Value Chain and Stack

Stablebanking isn’t just about a singular financial primitive such as issuing stablecoins or handling payments. It is about creating a composable financial stack where each component supports the others. From infrastructure to liquidity, each layer enables specific functions while contributing to the strength and flexibility of the overall system:

- Infrastructure layer: The foundation of Stablebanking, this layer includes stablecoin issuers, blockchains, and compliance tools. Issuers like Circle, Tether and Perena create stablecoins, while blockchains like Solana and Ethereum provide the rails for transactions. Compliance tools, such as Chainalysis ensure regulatory adherence, making Stablebanking transparent and secure.

- Wallet and custody layer: This layer enables secure storage and movement of stablecoins. Wallets (such as MPC-based solutions like Dynamic) and custodians (like Coinbase Custody) provide user-friendly interfaces and institutional-grade security.

- Application layer: Where Stablebanking meets real-world use cases, this layer includes payments (B2B, B2C, P2P), invoicing, payroll, and merchant transactions. Platforms like Superstate integrate stablecoins into neobanks, savings accounts, and subscription services, making them accessible to businesses and consumers.

- Liquidity and yield layer: This layer powers advanced financial services, including stablecoin swaps, cross-chain bridges, on/off ramps, and yield-generating products. Tools like Brale facilitate liquidity, while protocols like Ethena offer yield trading and tokenized real-world assets (RWAs).

Each layer is a building block, creating a “stablecoin sandwich” where value flows from issuance to custody to applications and liquidity, all onchain.

How the Layers Interact

The power of Stablebanking lies in its composability: each layer supports and enhances the others. For example:

- A stablecoin issued on Solana is stored in a Dynamic wallet

- A fintech uses this stablecoin for instant cross-border payroll, leveraging Chainalysis for compliance

- The recipient swaps the stablecoin for another asset via a cross-chain bridge or invests in a tokenized T-bill to generate yield

This seamless flow eliminates the silos of traditional finance, avoiding inefficiencies like delays and fees. This architecture is already reshaping global finance through:

- Cross-border payments: Near-zero fees and instant FX conversions for remittances.

- Institutional trading: Deep onchain liquidity for efficient, transparent markets.

- Emerging markets: Dollar-based stability for volatile economies, no bank account required.

- Integration with fintechs: Banks and fintechs adopting stablecoins to stay competitive.

This is just the beginning. The next evolution will combine stablecoin issuance with lending, trading, and asset management, giving rise to sophisticated financial institutions built onchain.

Perena: Pioneering the Stablebanking Revolution

Perena is building the first true Stablebanking network on Solana’s high-speed, low-cost blockchain. Their vision is a composable financial ecosystem where liquidity, payments, and yields flow freely across applications. By enabling open integration, Perena makes moving money simple, whether it’s for payroll, trading, or saving.

Comparing Circle, Tether, and Perena

Share